Social Security (SS), the nation’s safety net. Imagine where so many retirees would be without it. I know that my mom couldn’t even imagine retiring at the age of 70 without it. It covers the bulk of her living expenses. This is not an uncommon narrative. Looking out on the horizon, the future is not as certain for Social Security. That fact changes the plans of many young Americans. Today’s article from CNBC shows just how much doubt revolves around this benefit.

Quick History

The Social Security Administration (SSA) has a thorough history on their site, but I will hit some of the major points here.

Prior to any kind of pension program for citizens, all assistance was provided with extreme limitations. Recipients were mistreated, lost their property, right to vote and in some cases were made to wear a “P” on their clothing to express their status. This started to change after the Civil War when hundreds of thousands of American families lost their main breadwinner. The Civil War Pension Program from 1862 was the first prevursor to SS. It was specficlaly for disabled veterans and their widows/orphans. The benefits were then extended in 1906 to include old age as a qualification for veteran’s benefits. Shortly after, these benefits were expanded to all Civil War Veterans.

Generally, there has been a prerequisite of an extreme increase in need prior to government intervention to the status quo. The Civil War was the first and the Great Depression was the second event that created widespread need. The massive increase in job loss and poverty during the Great Depression spurred FDR on to pursue the Social Security Act of 1935. Even then, the program started with one-time, lump sum payments in 1937. The first monthly benefits started with a $22 check to Ida May Fuller, a VT resident, on Jan 1st, 1940.

Since 1940, there have been several expansions of the program. While the program is not perfect, it has objectively saved lives, kept many elderly citizens in their home and drastically improved women’s ability to work. If this program did not exist, many would have starved, been kicked out of their homes and would have required more caregivers, mostly women, to keep them comfortable.

Will Social Security Stick Around?

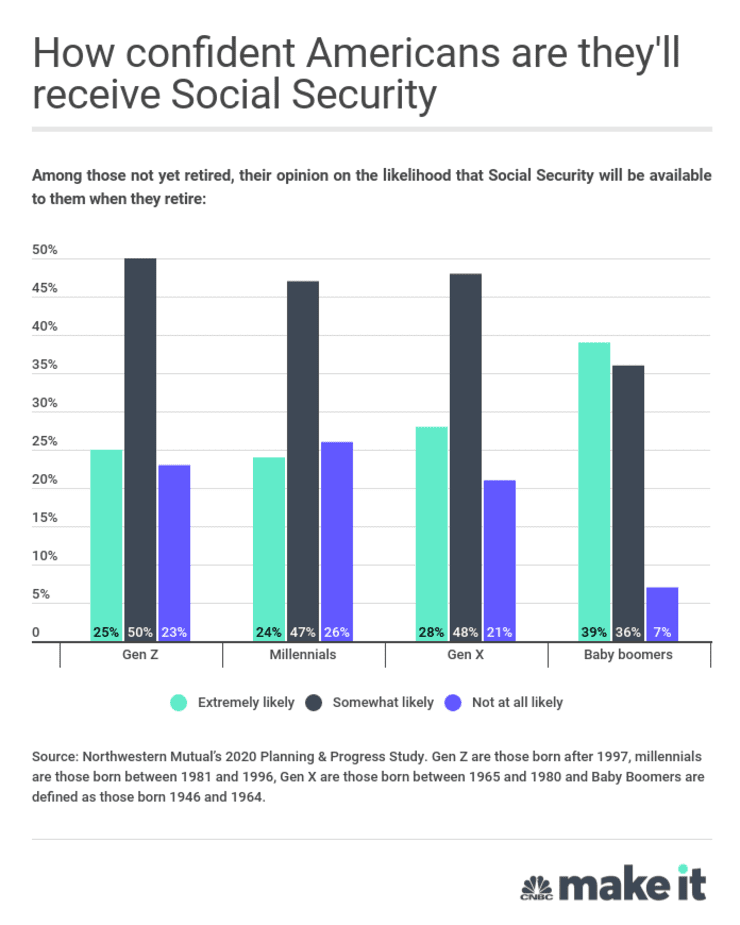

Unfortunately, there is a possibility that SS may not be available in the future, at least not in the same capacity, as it is for current retirees. Approximately 1 in 4 Millennials and Gen Z do not believe that SS will be there when they retire.

The reason for this concern is that with increased life expectancy has come increased costs in the program, which may not be covered by the current level of payroll tax that has been used in the past. This means that Social Security will have to start using reserve funds in order to cover a portion of benefits payments. Current estimates assume that reserves for the program could be exhausted in approximately 15 years.

While this may sound like Social Security will completely disintegrate at that time, that is not the case. If there are no changes to correct this issue over the next 15 years, SS would still be able to fund ~75% of planned benefits.

Of course, as with everything else, the pandemic made this problem worse. The massive job loss cut into the expected payroll taxes for the year. Additionally, the the low interest rates from the reduced earnings kept the reserves from generating the amount of interest expected for the year.

What Can I Expect?

Currently, Baby Boomers are expecting SS to cover 38% of their retirement. This is on average. There are many who will use their Social Security as their main source of income. The estimates for Gen Z and Millennials show that SS is expected to account for much less. Estimate are approximately 15% of total retirement savings will be made up of SS funds. This would mean that if you needed $5,000 per month in retirement spending, only $750/month could be expected from SS. To find out your total expected amount of benefits, go to ssa.gov and create an account. This number will update with each new year’s income statement from your tax returns.

Focus on What You Can Control

I’ve mentioned this before, but while what happens in the White house DOES affect your personal finances, you have to focus on what you can control. One of the best things you can do is to front load your retirement. In order to make up any reduction in SS benefits, individuals will need more retirement savings.

For example, opening up an employer sponsored retirement accounts, such as 401K/ 403B /457 plans or increasing your current contributions. Otherwise, there are other retirement accounts such as SEP IRAs, SIMPLE IRAS, Roth and Traditional IRAs. If all of this sounds a bit confusing, I recommend working with someone like a financial coach or a fee only financial planner.

Sometimes, increasing your retirement savings is not an option at this time. First, I would recommend working with a financial coach to bring in a third party to take a look at your finances from a different point of view. However, if that is still the case, there are other options that can be walked through. Perhaps you could find a less stressful, part time job for the first several years of your retirement to reduce your risk.

One critical step, no matter your current retirement savings is to set up your estate plan. An estate plan ensures that your wishes are considered in a clear state of mind. This includes how you want to age, how you want to be cared for in case of incapacitance and more. If this isn’t something that you’ve thought about check out this free resource. I detail steps you can take to create your estate plan and help those around you.

Remember, that taking personal action doesn’t mean that laws do not need to change, but both need to be done at the same time. The wheels of government spin slowly. Don’t put your life on hold while waiting and pushing for Congress to act. Use your money as a tool to build the life you deserve.

What is your current plan? Do you have one? Let me know in the comments below!

Leave a Reply