5 Tips for Buying a Car the Smart Way

As part of Focused Frugal February, I wanted to talk about another of the “big three” expenses for the American household. Transportation. Specifically, I wanted to talk about buying a car since most of America was not built with public transportation in mind. Today’s Money in the Media Monday article comes from NPR, called “5 Tips for Buying a Car the Smart Way“

A couple of notes before we jump in. First, these tips are specific to buying a car from a dealer. If you’re looking at a private market, my main advice to you is to make sure you have a mechanic you trust take a look at the car before you buy.

Second, some of these tips specifically relate to the financing side of the car buying process. Obviously, the best thing to be able to do would be to buy a car with cash. I realize that this isn’t a viable option for everyone, especially if you need to obtain a car quickly. If you are able to buy a car with cash without sacrificing your emergency funds, do it! Otherwise, the finance related tips are very useful to help you get a good car that you can pay off quickly.

Finally, the last bit of advice before we get into NPR’s advice is to make sure that you are aware of any tricks a shady dealer may try to pull. There are plenty of reputable businesses out there, but there are also a lot of shysters. Be vigilant and double check any and all paperwork before you sign it. So, without further ado, let’s get into it!

Get Pre-Approved

This advice breaks down one of the dealer’s tricks before you even walk onto a lot. Knowing how much you are approved for by an outside lender causes you to take the time to look at the cold hard numbers before the salesman works their magic and shows you a shiny new car with all the bells and whistles.

Knowing not just the amount that you’re approved for, but the interest rate and your credit score will help you tremendously in the bargaining process. This is especially true if you have time on your side and are able to build up your credit score prior to looking into buying a car. It’s also a good idea in general to check your score just to make sure that there are no errors prior to making such a large purchase. Getting a better rate can save you a LOT over the course of a loan.

This article also mentions that a dealer may offer you a rate, either higher (not knowing you’re pre-approved for lower) or lower (trying to get you to finance with them) than what you have been pre-approved. Be careful with this, if they offer you higher, clearly the response is to decline. If they go lower, be sure that they are a reputable company before getting into financial dealings with them. Preferably a major bank or dealer would be best for financing.

Keep it Simple

Part of the game that dealers play is to talk about all of the various negotiation points at once. This is a trick to make you confused and they do it because it works. Why does it work? It works because humans are not meant to multi-task so be wary.

The first step would be to focus on the price of the actual vehicle without taking into account any trade-ins or loan criteria. The dealer will try to bring those items into the conversation, but stay firm. “We’ll get there. I just want to talk about how much this car costs right now,” is a perfectly acceptable thing to say.

If you negotiate a really good purchase price on the car, they might jack up the interest rate to make extra money on you that way or lowball you on your trade-in. They can juggle all those factors in their head at once. You don’t want to. Keep it simple. One thing at a time.

After the price has been decided, then bring in other elements like a trade. There’s work to be done on this before getting to the dealer as well. You’ll want to use at least one, if not more of the free tools available to you to get a fair value on your car. Some of tools can be:

One of the most important things that I’ve found in all negotiations was sort of a throw away line in this article.

You have to be willing to walk away.

If you feel that the car price or the trade in value they’re offering are not in the range you know to be fair, then walk. There are plenty of other cars and dealerships that will be willing to negotiate.

Don’t Buy Any Add-Ons

This goes along with what was stated above. Keep it simple. All of the add one can be extremely overpriced. As with most industries, it’s in the aftermarket that they make their money. Here are some of the things, the financial manager might try to sell you on:

- Extended warranty

- Gap insurance

- Tire protection plan

- Paint protection plan

- Anything else they think you might buy

Of these two items, the two that may have some merit are the extended warranty and gap insurance. However, this article makes a great point that if you do want the extended warranty, you can always get it towards the end of your regular warranty. What you don’t want to do is roll it into your loan and pay interest on the cost of that warranty.

As for gap insurance, I agree with the sentiment that this is something that you would want to pursue from your insurance company and not through a dealership.

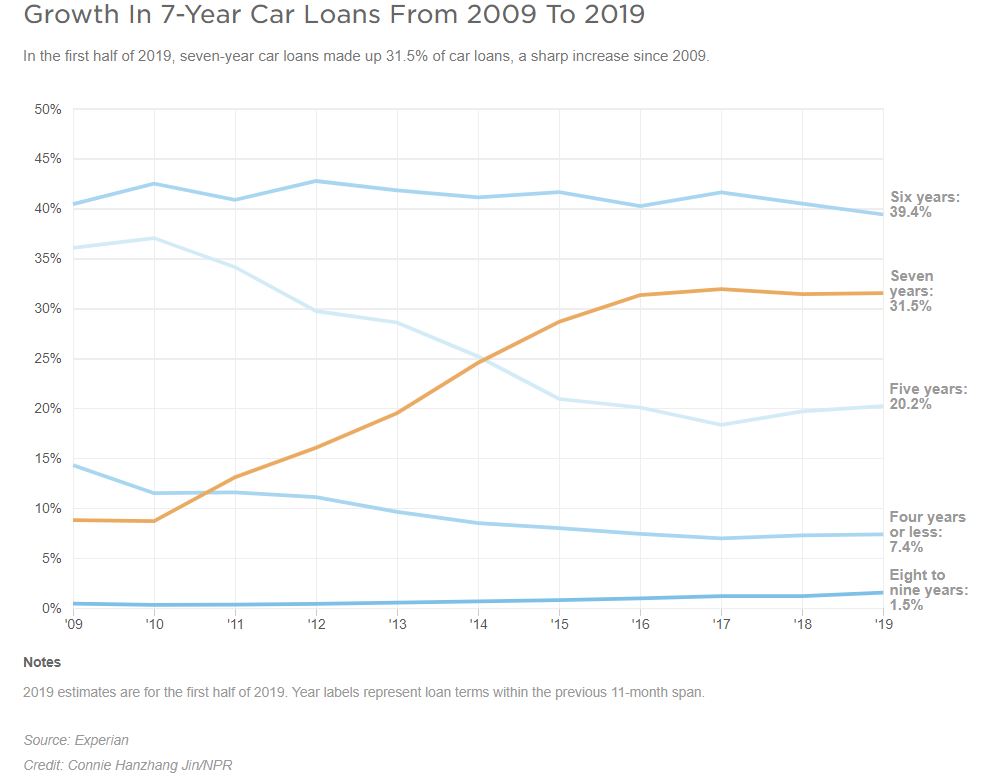

Longer Term Loans Are NOT Better

This is part of the reason why you negotiate the overall price of the car before you negotiate financing. Longer loan terms have become a common way for dealers to get more money for the same car. Sure a lower payment sounds nice, but when you’re paying it for 7 years it quickly loses it’s sheen.

Even worse, these 7 year loans have higher interest rate than the traditional five year loan. Meaning that in the beginning of the loan, you’d be paying more interest than principal. This, coupled with the fact that 33% of Americans roll $5,000 in debt into their new car purchases are what create the perfect storm to be underwater on a new vehicle.

Buy What You Can Afford. Also, Used is Better

This advice is one of the most important because if you don’t get this part right. None of the rest really matters. The rule of thumb for car expenses is that they shouldn’t consume more than 20% of your take home pay. Personally, I think that’s quite a bit, but I won’t fight this article on that point at least here.

To hold to this “rule”, the car payment shouldn’t be more than 10-15% of your total take-home pay. This part makes sense since the car payment is really just the beginning for costs on a car. There’s insurance, gas, maintenance and taxes to consider. For the latter two costs, I highly recommend a sinking fund to prevent these expenses from being an unwelcome surprise.

Along the same lines of buying only enough car as what you need, the recommendation always stands to buy used. We personally are planning on the rest of the cars we buy to be used. I’d previously bought a new car and will never buy new again. It just wasn’t worth the extra cost to me because a brand new car doesn’t align with my values.

So, I will ask you, where you your values lie? Does a new car fit in with those values or would you want that car payment to go towards something else? Your retirement? Your child’s college fund? Maybe a dream vacation? The choice is yours, but regardless on if you buy new or used, take these tips along with you to ensure that your next car buying adventure is a success.

Are you in the market for a new (to you) car? Is the car you have more payment than you can handle? Or have you bought a car recently and had a successful or unsuccessful experience? Let me know in the comments below!