Last month I discussed budgeting for your vacation. This is great in allowing you the freedom to take time for yourself while still paying off debts, particularly when you have a long payoff journey (ours was about 8 years). The strategy to create these various buckets of money is called Sinking funds and they’re not just for vacations.

What exactly is a Sinking Fund for?

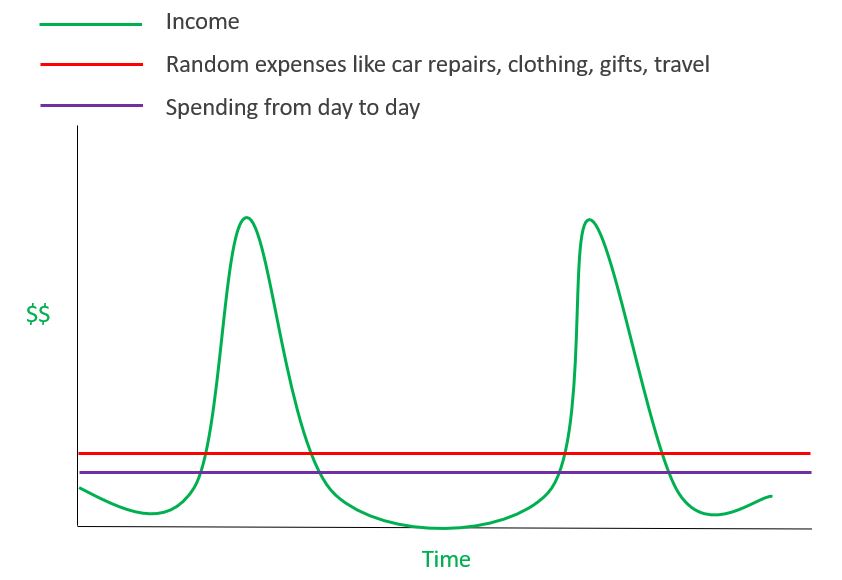

To start off, a sinking fund is money that is planned to be spent on an expected occasional or random expense. Expected occasional expenses are ones that you are aware of, but they are due at a regular interval that is not monthly. For example, you may have your insurance premium due every 6 months. While a random expense is something that you expect, but are uncertain of when it will occur. A good example of this is a car or home repair.

A sinking fund takes these irregular expenses and levels them out in order to turn them into regular monthly expenses.

While having an emergency fund will keep you from going into debt should an actual emergency occur, sinking funds will help you live a proactive financial life. How many times have you saved up an emergency fund and then had something come up to have to dip into it? Every flat tire or large vet bill then becomes a reason to rob your emergency fund, leaving you exposed.

How to Create a Sinking Fund?

Sinking funds are best utilized when they’re kept in a separate account to ensure that they can be saved for that specific purpose. Here are some examples of what sinking funds we have set up:

- Travel- Flights, Hotels, Food costs when on vacation

- Car Fund- Maintenance, Registration, Taxes

- Clothing

- Pets- Vet Bills, Food, Toys

- Gifts- Birthdays, Holidays, Special Occasions

- Disability Insurance– For the annual premium payments

Once the separate savings account is set up, the amounts for monthly deposit need to be determined. As an example, I’ve just reassessed the amount that we currently save for our pets. I wasn’t sure what to add to this account at first and so, I chose $75.

After several months, I noticed that this was staying near zero just from smaller expenses, like food, Heartgard, etc. I realized that if I had a larger expense, say a vet visit, that I would not have enough saved for this expense. So, I did a deep dive into our pet expenses. We buy all of our food and most other accessories on Chewy so it was simple to pull up all of our normal expenses from the last several months.

Then I grabbed the last few vet bills that I had received and added these to my totals. From there, I realized that we spend about $1,800 on our three pets every year. Breaking this down, that is $150/month. Meaning that I was underestimating our pet expenses by half! Now, I’m confident in the amount that we save for our pets and will continue to check in on our other accounts every few months to do the same analysis.

Wrap It Up!

Not only has creating these sinking funds prevented us from spending money that we would need for future occasional and random expenses, it caused us to reevaluate our current budget. Taking a look at each line item that required a sinking fund and doing the math to determine if we were on the right track for our budgeted amounts. In the case of our pet fund, we were way off and had to double what we contributed every month.

We will now take that lesson and reevaluate how we are doing every month for these accounts and update our budgeted contributions as needed. It’s a good reminder that budgets are ever-changing as life changes. Taking the time to reevaluate will help keep you on top of your goals.

Do you use sinking funds? What categories do you use them for? Let me know in the comments below!

[…] a quote from the plumber and knew that we had at least that much saved in our home maintenance sinking fund. What are sinking funds? They are accounts where you can put smaller amounts of funds on a monthly […]

[…] part of this budgeting exercise, set up automatic transfers to sinking fund accounts. These would accounts for items like car maintenance/ taxes/ registration, clothing, […]

[…] was the trip of a lifetime. We saved up for this trip in our travel sinking fund over the course of several years and then delayed another year due to COVID-19. It was only once we […]