With the onset of fall comes apple picking, jumping in leaves, pumpkin patches and healthcare enrollment! All of these things are clearly equally as fun. So, let’s just dive right in and take a look at where you’d even get started.

What Are Your Options?

If you have employer provided healthcare or not, the first step is to gather up all of your options for healthcare. These could be:

- Your employer

- Your spouse (or domestic partner)’s employer

- ACA marketplace

- State marketplace that may offer state specific plans

- COBRA

- Medicaid/Medicare (if eligible)

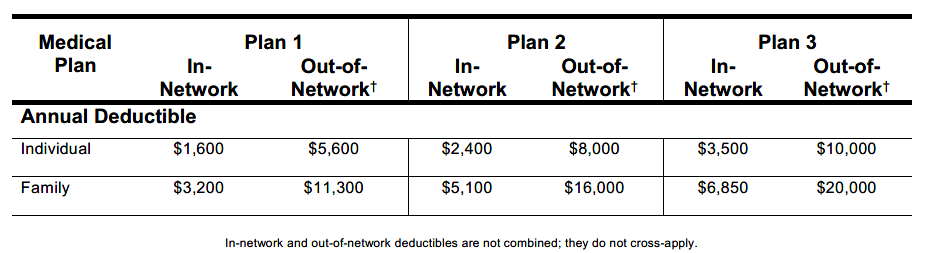

Each of these plans should have a summary sheet explaining the benefits. Here is a sample of that from one of the healthcare plans my employer offers:

What Do You/Your Family Need?

What did we spend last year and so far this year on healthcare?

This can be a good indicator of what you’d expect to spend for the coming year. In our case, we spent ~$300 for the year on medical costs (dental and vision are separate), so it doesn’t make sense for us to pay for the most expensive plan when that deductible is still $1,400. We luck out here because we are young and healthy to be able to take the risk of the higher deductible plan.

Are there any expected changes in our circumstances for next year?

Your expenses from last year could be a good measure for a baseline or specific circumstance if something occurred during the year. However, if you have a completely new event (pregnancy or recent issue where you think you may need surgery next year), then you will want to look up how much those things can cost in order to determine which plan best fits your situation.

If we have an unexpected medical expense, could we pay for the max out of pocket cost?

This question is one that not many actually look at, but it is crucial to ensure that should something happen, there is a plan in place. The out of pocket maximums can be quite large, so this is important to take into account.

Rinse and Repeat

This method will need to be used for Dental and Vision plans as well. These plans tend to be much cheaper than medical and are worth it, especially if you have problems with your teeth or eyes.

It Pays to Be Healthy

As you can tell from the plans I showed that are offered at my current employer, the costs can be vary minor or many thousands of dollars. If you are lucky enough to currently be healthy, then do everything that you can to remain so by taking care of yourself throughout the year.

- Go to those annual preventative doctor appointments

- Eat healthy

- Exercise

- Get the proper amount of rest

- Drink more water- specifically calling out my wife on this one.

On a final note: Do not sacrifice health in the name of frugality as it literally costs less to be healthy.

By this I mean, don’t just go for the cheaper plan because it is cheaper, evaluate what is the best option for you and your family. Don’t eat unhealthy foods, if you can afford something better just to increase your savings. The payoff for being healthy will far exceed the cheaper costs you see today both in actual dollars and overall quality of life.

Part 2 Preview

In Part 2 to come out next Friday, I will deep dive into various ways to save and pay for the varying medical costs that come up in our lives.

Are you ready for open enrollment? Do you have questions on the various plans you are eligible? Let me know in the comments below!

Leave a Reply